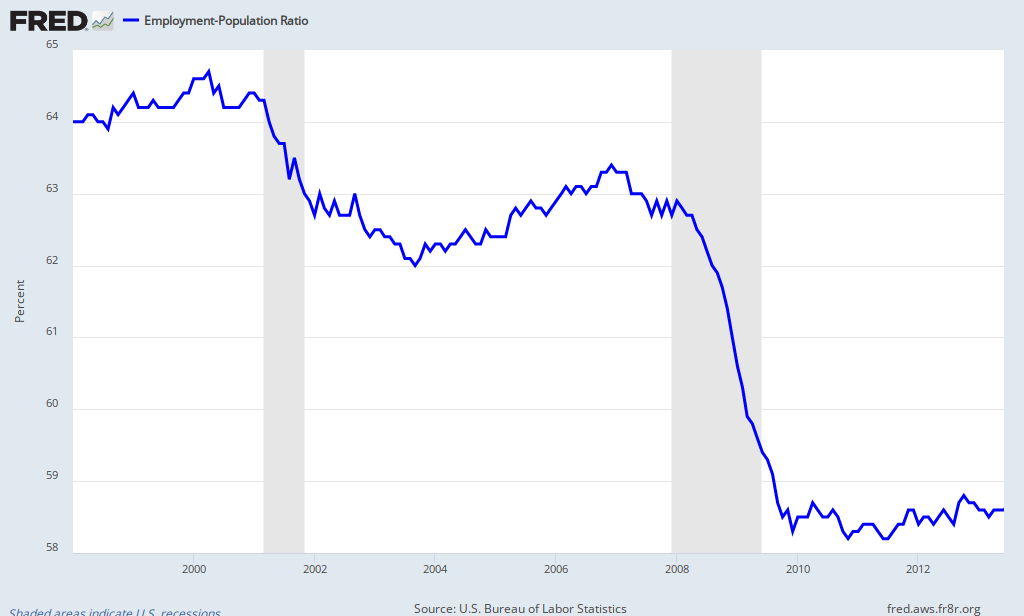

In fact, while US productivity soared, "[w]ages have fallen to a record low as a share of America’s gross domestic product. Until 1975, wages nearly always accounted for more than 50 percent of the nation’s G.D.P., but last year wages fell to a record low of 43.5 percent. Since 2001, when the wage share was 49 percent, there has been a steep slide." This basic loss of buying power (relative to output) for workers combined with loss of bargaining power for wage increases creates a powerful deflationary bias in our economy. Just look:

As The Economist notes: "The core PCE number (personal consumption expenditure deflator) is only 1% - a modern low - and the Dallas Fed, which uses a trimmed mean number (eliminating the outliers), actually recorded a small fall in the latest numbers (see the definition here)."

In the face of all this evidence of deflationary forces, the US now assumes a contractionary fiscal policy due to the mindless sequestration and the Fed is talking about tapering-off its monetary stimulus. Both fiscal and monetary policy now look strongly contractionary in the US.

Economic stagnation looks worse in other parts of the world. In the Eurozone unemployment recently reached an all time high of 12.2 percent which flirts with outright depression. Some areas of the Eurozone are already in deep depression with only bleak prospects ahead. In Spain, unemployment hovers at 27 percent. I blogged recently about the biggest basket case in Europe (Italy) but in fact austerity has failed everywhere and southern European debt burdens have increased not decreased as the eurocrats promised. Politically, disruptions could erupt at any minute across the Eurozone, as Spain is reportedly in a pre-revolutionary state and even France is fraying. Just this week Portuguese debt yields spiked to highs not seen for months; this signals real problems ahead in the Eurozone.

Then there is China. The world's second largest economy is clearly slowing down. China recently experienced a dramatic credit crunch that suggests its banking sector is overextended. Some experts see major problems ahead. At the very least, China is losing steam and cannot support global growth anytime soon.

“Japan’s economy is starting to recover moderately.” But, the problem here is that Japan is already in a deflationary spiral and prices only stopped falling in May. This progress all comes at the expense of the rest of the world which suffers as Japan drives down the value of the Yen and exports deflation. It is not internally generated growth as the rest of the world recognizes. As the Yen declines (20 percent in just 8 months), Japan can effectively flood the world with cheap goods. As one expert states: "Forget cars, Nintendo machines or anime. Japan’s biggest export right now is deflation."

So, looking at all the world's biggest economies, it is hard to remember more deflationary pressures than right now. Certainly, not since the summer of 2008 did the global economy seem more vulnerable to a major shock.

No comments:

Post a Comment